Common Reasons Windshield Claims Get Delayed or Denied

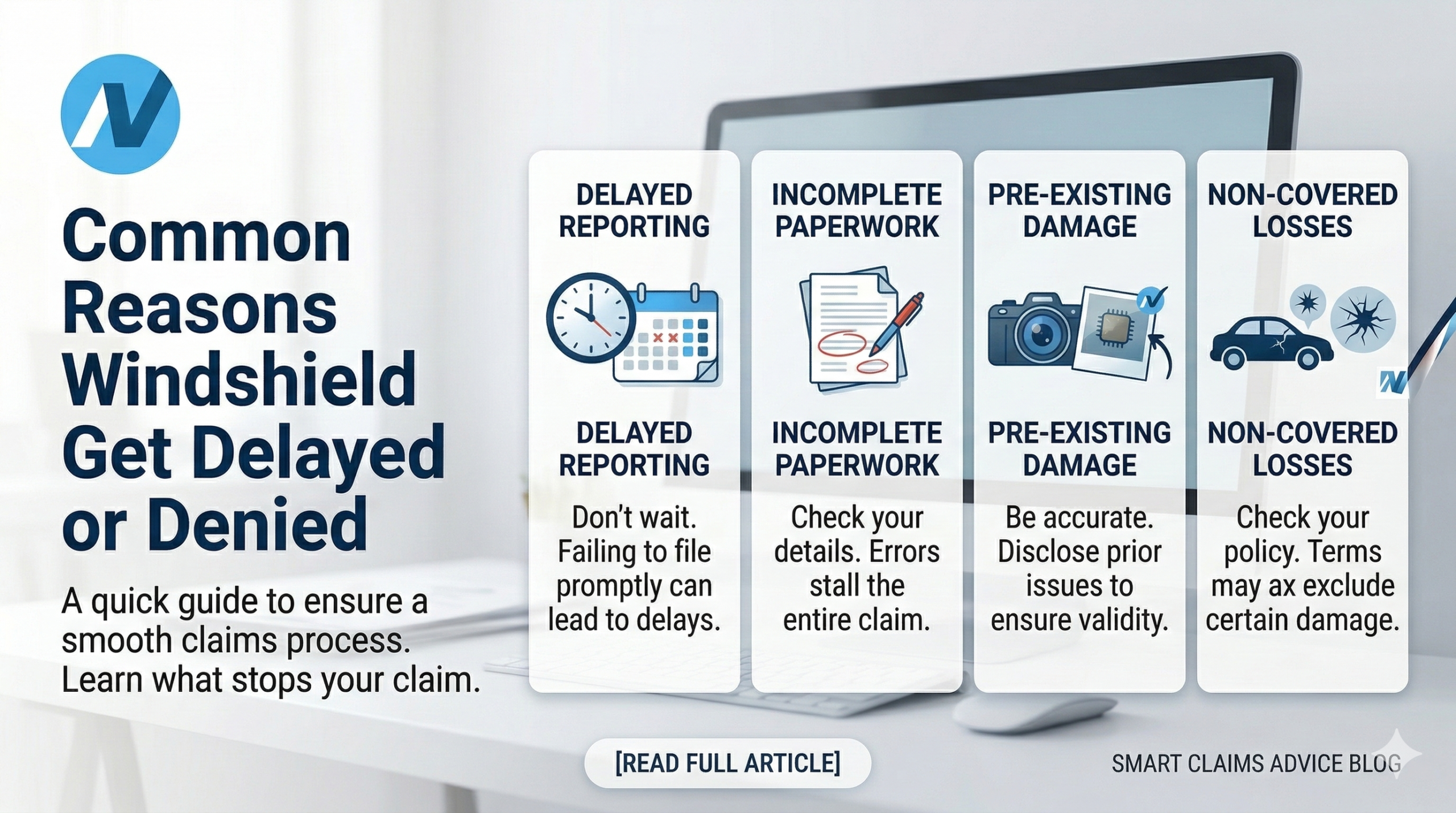

Windshield insurance claims get delayed or denied for five primary reasons: pre-existing damage questions (35% of denials), policy coverage disputes (25%), insufficient documentation (20%), suspected fraud (15%), and policy exclusions (5%). The most critical factor across all five categories is proving damage occurred during active policy coverage with clear dated photos and accurate descriptions.

The good news: 80 to 90% of claim problems are preventable. And most denials are appealable with proper evidence.

This guide covers each denial category in detail, what triggers them, how to prevent them, and what to do if your windshield replacement or repair claim gets rejected.

| Denial Reason | % of Denials | Preventable? | Typical Delay Added |

|---|---|---|---|

| Pre-existing damage questions | 35% | Yes, with documentation | 3-5 days |

| Policy coverage disputes | 25% | Yes, with verification | 5-10 days |

| Insufficient documentation | 20% | Yes, completely | 1-3 days per resubmission |

| Suspected fraud | 15% | Partially | 10-20 days |

| Policy exclusions | 5% | Yes, by reading policy | Permanent denial (appeal possible) |

Why Do Insurers Deny Claims for Pre-Existing Damage?

Pre-existing damage is the single biggest reason windshield claims get denied, accounting for roughly 35% of all rejections. Comprehensive coverage only covers damage that occurs during the active policy period. If the insurer suspects the crack or chip existed before coverage began, they’ll deny the claim.

Common Scenarios That Trigger This Flag

Recent policy addition: You added comprehensive coverage this month, then filed a glass claim within 30 days. From the insurer’s perspective, the statistical correlation between coverage changes and immediate claims suggests the damage may have existed before the coverage did.

Policy shopping: You switched insurers and filed a claim shortly after your new policy started.

Coverage restoration: Your comprehensive coverage lapsed, you restored it, and filed a claim soon after.

All three scenarios look the same to an insurer’s fraud detection system, regardless of whether the damage genuinely happened post-coverage.

How to Prevent Pre-Existing Damage Denials

Document your windshield condition when adding coverage. Take dated photos showing no damage the day your new policy starts. This single habit eliminates the most common denial reason entirely.

Wait 45 to 60 days after coverage changes before filing. This reduces the fraud perception. It doesn’t eliminate your legitimate claim rights, but it avoids triggering automated screening.

Maintain continuous coverage. Avoid gaps that create questions about damage timing.

Be honest about damage discovery. If damage genuinely occurred post-coverage, an accurate timeline with supporting evidence protects your claim.

If You’re Denied for Pre-Existing Damage

Challenge the decision with dated photos, witness statements, and a clear damage discovery timeline. Request the specific evidence the insurer used to determine the damage was pre-existing. File a formal appeal, and if that fails, contact your state insurance department.

What Causes Policy Coverage Disputes?

Coverage disputes account for 25% of windshield claim denials. These happen when there’s a disconnect between what you think your policy covers and what it actually covers at the time of damage.

| Coverage Issue | What Happens | Prevention |

|---|---|---|

| Comprehensive coverage lapsed | Missed payment or cancellation you didn’t notice | Set up autopay; verify coverage status quarterly |

| Collision vs. comprehensive confusion | Damage from an accident filed as comprehensive instead of collision | Understand claim type before filing |

| Excluded driver | Person driving during damage event isn’t listed on policy | Add all regular drivers to policy |

| Vehicle not covered | Damage to a vehicle not on the policy (borrowed, recently bought) | Update policy immediately when acquiring vehicles |

The most common version we see: a driver thinks comprehensive coverage is active but missed a payment that triggered a lapse. Always verify your coverage status before filing. A 2-minute call to your insurer can save you a 10-day dispute.

If denied for coverage reasons: Review your policy declarations page. Check your payment history to confirm no lapse occurred. Request the insurer provide proof of the coverage gap on the specific date of damage. If the damage happened during an accident, consider filing under collision coverage instead.

How Does Insufficient Documentation Lead to Denial?

Documentation failures account for 20% of denials and are the most preventable category. These aren’t real denials in the traditional sense. They’re claims that stall because the insurer doesn’t have enough information to process them.

What Insurers Actually Need

| Required Documentation | Good Example | Bad Example |

|---|---|---|

| Damage photos | Multiple angles, close-up + wide shot, good lighting | One blurry photo from 10 feet away |

| Damage description | “6-inch diagonal crack starting 4 inches below rearview mirror, extending toward passenger side” | “Cracked windshield” |

| Dated images | Timestamped photos proving when damage was photographed | Undated photos with no context |

| Vehicle details | Year, make, model, VIN, policy number | Missing VIN or wrong policy number |

| Damage timeline | “Noticed chip on March 3 during morning commute on I-10” | “Found it sometime last week” |

Each resubmission due to missing info adds 24 to 48 hours. Two incomplete submissions can turn a 24-hour approval into a week-long process.

The fix is simple: take comprehensive photos immediately (wide shots and close-ups), note the date, time, and circumstances of damage discovery, and provide a detailed written description with your claim. Submit the complete package upfront. Don’t wait for insurers to request what’s missing.

Professional glass shops handle this routinely. NuVision documents damage to insurer standards as part of every claim we file, which eliminates documentation-related delays across Arizona, Florida, South Carolina, and Colorado.

When Do Fraud Flags Get Triggered on Legitimate Claims?

Suspected fraud accounts for 15% of windshield claim denials. Between 10 and 20% of all insurance claims nationally involve some level of fraud, which means insurers have built aggressive automated detection systems. The problem: legitimate claims sometimes get caught in those filters.

What Triggers Fraud Screening

Suspiciously timed claims: Coverage added recently, claim filed within days.

Claim frequency patterns: Multiple comprehensive claims across a short timeframe (4+ in 3 years raises flags).

Inconsistent information: Photos that don’t match the written description. Timeline that doesn’t add up.

Claim stacking: Multiple unrelated damages reported simultaneously.

When Legitimate Claims Get Flagged

Drivers in debris-heavy areas (highway commuters in Phoenix, Mesa, Scottsdale) legitimately experience frequent glass damage. Arizona’s claim frequency runs 22 to 28% of insured vehicles filing glass claims annually, compared to 12 to 15% nationally. Multiple legitimate claims in a short period can still trigger fraud filters even when every claim is genuine.

Honest reporting errors also cause flags. Minor inconsistencies from memory lapses (getting the exact date wrong by a day, misremembering which highway you were on) can look like intentional deception to an automated system.

If denied for suspected fraud: Provide clarifying information thoroughly and honestly. Offer additional evidence like witnesses, location details, and supporting documentation. Request a formal review by a senior adjuster. If the insurer persists with unfounded allegations, seek legal advice.

Important: Insurance fraud is a serious crime. Never fabricate or exaggerate damage, misrepresent timing, or file false claims. Honest reporting is your strongest protection against fraud allegations.

What Policy Exclusions Can Block a Windshield Claim?

Policy exclusions account for only 5% of denials but result in the hardest denials to overturn because they’re typically valid.

Intentional damage: You or a household member deliberately damaged the windshield.

Illegal activity: Damage occurred during commission of a crime.

Commercial use exclusion: Personal auto policy doesn’t cover commercial vehicle use. Rideshare drivers and delivery drivers frequently hit this exclusion.

Excluded vehicle types: Classic cars, heavily modified vehicles, or specialty vehicles may have coverage limitations.

Prevention: Read your policy exclusions before you need them. Verify your vehicle use classification matches your actual use. Disclose modifications. If you use your vehicle commercially, confirm your policy covers that use.

How Do Denial Patterns Differ Across Arizona, Florida, and South Carolina?

Each state’s insurance market creates distinct denial patterns that drivers should understand.

Arizona

Denials are relatively rare due to the established zero-deductible market. When they happen, coverage disputes (lapsed policies) are the primary cause. The high claim volume (85% of policies include glass coverage) means insurers have streamlined processes that catch fewer legitimate claims in fraud filters.

Arizona’s cashback offers ($375 at NuVision) are legal marketing incentives separate from insurance and don’t affect claim validity. Drivers in Chandler, Phoenix, Mesa, and Scottsdale benefit from the most established glass claims infrastructure in the country.

Florida

Post-SB 1002 (signed May 25, 2023), increased scrutiny has reduced fraud but created more documentation requirements. The law eliminated assignment-of-benefits for auto glass claims, meaning shops can no longer file on your behalf without explicit customer authorization. This added verification step catches some legitimate claims that miss the new authorization requirement.

Repair vs. replacement disputes are more common in Florida. Insurers prefer repairs because the statutory deductible waiver applies to repairs specifically. If you need full replacement, the insurer may push back harder. Drivers in Tampa, Orlando, Miami, and Jacksonville should understand the repair vs. replacement distinction before filing. For more on Florida’s coverage structure, see our zero-deductible windshield replacement guide.

South Carolina

Standard insurance market denial patterns apply. Pre-existing damage questions are slightly more common in rural areas where delayed shop access means longer gaps between damage occurrence and claim filing. Overall denial rates remain lower than the national average due to traditional, established processes.

Drivers in Charleston, Columbia, Greenville, and Myrtle Beach benefit from consistent processing but should document damage immediately to avoid pre-existing damage questions that arise from delayed filing.

How Do You Appeal a Denied Windshield Claim?

Most windshield claim denials are appealable. Here’s the process step by step.

Step 1: Request a written denial explanation. The insurer must provide the specific reason for denial, the policy provisions they’re citing, and the evidence they relied on. Don’t accept a vague phone explanation. Get it in writing.

Step 2: Review the denial validity. Compare the denial letter against your actual policy terms. Verify the insurer’s interpretation is correct. Gather any contradicting evidence if the denial seems unjustified.

Step 3: File a formal appeal. Submit within the specified timeframe (typically 30 to 60 days). Provide additional documentation supporting your claim. Request reconsideration at the supervisor level. Include everything that contradicts the denial reason.

Step 4: File a state insurance department complaint. If the appeal fails, escalate to your state regulator. They investigate unfair denials and can compel insurers to reconsider.

| State | Regulatory Body |

|---|---|

| Arizona | Department of Insurance and Financial Institutions |

| Florida | Department of Financial Services |

| South Carolina | Department of Insurance |

| Colorado | Division of Insurance |

Step 5: Legal options (last resort). Consult an insurance attorney. Consider small claims court for disputed amounts. Evaluate whether the cost of legal action makes sense relative to the claim value. For standard windshield claims ($300 to $1,200), the appeal process typically resolves the issue before legal action becomes necessary.

How Can You Prevent Windshield Claim Problems Before They Start?

Proactive documentation prevents the vast majority of delays and denials. Here’s the checklist that covers all five denial categories.

Before damage happens: Photograph your windshield condition when starting a new policy. Verify comprehensive coverage is active. Understand your deductible (or zero-deductible status). Read policy exclusions. Confirm vehicle use classification matches reality.

When damage occurs: Take multiple clear photos immediately from different angles. Note the date, time, location, and circumstances. Don’t wait days or weeks to document. The longer the gap between damage and documentation, the more questions arise.

When filing: Have your policy number, VIN, and insurance contact ready. Provide a detailed description with specific measurements and location on the windshield. Submit the complete package upfront. File Tuesday through Thursday between 9 AM and 2 PM for fastest processing.

Let an established shop handle it. This is the single most effective prevention strategy across all five denial categories. NuVision’s claims team knows exactly what documentation each insurer requires, the submission formats that avoid processing delays, and the follow-up timing that keeps claims moving. We file claims in the insurer’s preferred format with complete documentation from the start. For a full walkthrough of the filing process, see our guide on filing a windshield insurance claim.

Does a Denied Claim Affect Your Ability to File Future Claims?

A single denied claim generally doesn’t affect your ability to file future claims or your premium. The denial simply means that specific claim wasn’t approved.

However, a pattern of denied claims can create problems. Multiple denials within a short period may flag your account for additional scrutiny on future claims. Denied claims that involved fraud investigations (even if you were cleared) may remain in your claims history database (CLUE report) for up to 7 years.

The best protection: file legitimate claims with complete documentation. If a claim gets denied, appeal it properly rather than abandoning it and filing a new one for the same damage. For more on how claims interact with premiums, see our guide on how filing a windshield claim affects your insurance.

Frequently Asked Questions

Can I still get my windshield replaced if my claim is denied?

Yes. A denied claim means insurance won’t cover the cost, but you can still pay out of pocket. NuVision offers competitive cash pricing for windshield replacement across all service areas. For a breakdown of costs without insurance, see our windshield replacement cost guide.

How long do I have to appeal a denied claim?

Most insurers allow 30 to 60 days for formal appeals. Check your denial letter for the specific deadline. Don’t wait until the last day. File as soon as you have your supporting documentation assembled.

Will NuVision help with the claims process even if my claim was denied?

Yes. Our claims team can review the denial, identify what documentation might strengthen an appeal, and resubmit on your behalf. We handle claims across Arizona, Florida, South Carolina, and Colorado.

Does filing a windshield claim raise my insurance rates?

Typically no. Windshield claims fall under comprehensive coverage and are treated as no-fault events. Most insurers have “glass claim forgiveness” policies. Filing 4+ claims in a short period could flag your account, but a single claim almost never affects premiums.

Can the insurer force me to repair instead of replace?

Insurers can recommend repair over replacement, but the final determination depends on damage severity and safety standards. If the damage exceeds repair criteria (typically cracks longer than 6 inches, damage in the driver’s direct sight line, or compromised structural integrity), replacement is the appropriate remedy. In Florida post-SB 1002, repair vs. replacement disputes are more common because the statutory deductible waiver applies specifically to repairs.

What if my ADAS-equipped vehicle claim gets denied?

ADAS calibration is increasingly recognized by insurers as a required component of windshield replacement on equipped vehicles. If the calibration portion is denied, request the insurer cite the specific policy provision excluding it. Most comprehensive policies cover all necessary components of windshield replacement, including calibration. Whether you drive a Toyota, Honda, Ford, Tesla, or Chevrolet, calibration documentation from NuVision supports the claim that the service was necessary. Learn more about the process in our ADAS calibration guide.

Should I pay out of pocket for small damage instead of filing a claim?

Consider it if the repair cost ($75 to $150) is close to or below your deductible. Filing a claim for an amount barely above your deductible adds a claim to your history without meaningful financial benefit. In Arizona where zero-deductible coverage is standard, there’s no reason to skip filing. In Florida and South Carolina, weigh the repair cost against your deductible.

NuVision Prevents Claim Problems Before They Start

We file thousands of windshield claims across four states every month. Our claims team knows the documentation standards, submission formats, and follow-up timing that prevent delays and denials. When you work with NuVision, we handle the entire process: documentation, filing, insurer communication, and appeal assistance if needed.

Get a Free Quote and Start Your Claim →

Dealing with a denied claim right now? Our team can review the denial and help build your appeal. Call 1-855-213-0100 or request a quote online.

Mobile service available throughout Arizona, Florida, South Carolina, and Colorado. Whether your claim is approved or you’re paying cash, we come to you.