Zero-Deductible Windshield Replacement: Is It Really Free?

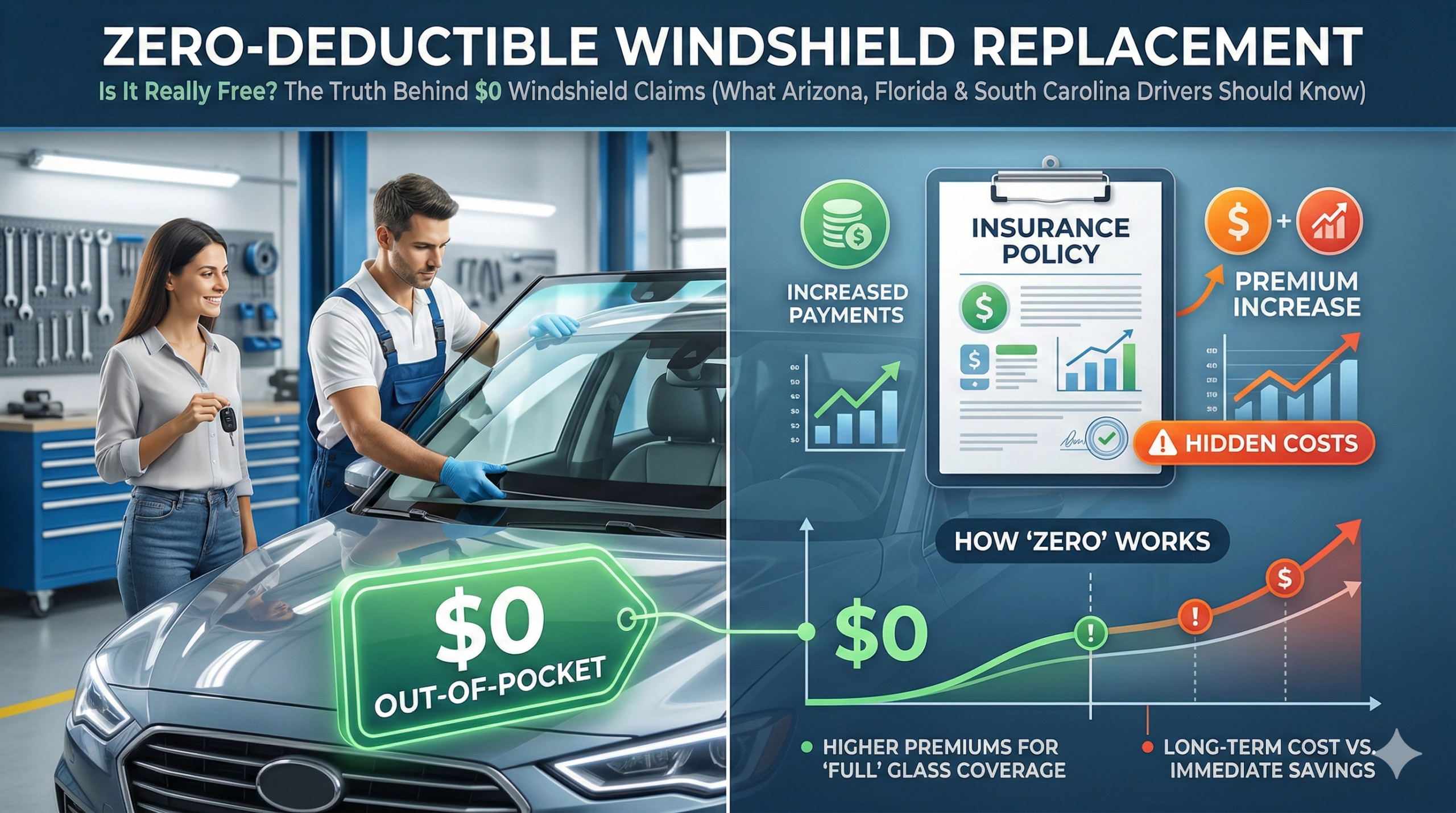

Zero-deductible windshield replacement means you pay $0 out-of-pocket when your glass gets replaced. But it’s not truly “free.” The cost is baked into your insurance premiums — either embedded automatically (like in Arizona, where 85% of comprehensive policies include it standard) or purchased as an add-on endorsement in states like Florida and South Carolina. Arizona drivers pay roughly $40-80 per year through embedded premiums. Florida and South Carolina drivers pay $40-150 annually for explicit glass endorsements.

So is it worth it? For most drivers in debris-heavy, extreme-weather states — absolutely. Zero-deductible glass converts unpredictable $300-1,200 windshield replacement costs into small, predictable annual premium increases. This article breaks down the real economics, state-by-state value analysis, hidden costs, and when zero-deductible coverage genuinely pays for itself.

How Does Zero-Deductible Glass Coverage Actually Work?

Insurance runs on risk pooling. Everyone pays premiums. Those who experience losses get payouts. Zero-deductible glass works the same way — except instead of paying a $500 deductible at claim time, you pre-pay a smaller amount annually through your premium. Whether you file a claim or not.

Here’s how insurers price it. They look at historical data — in Arizona, 22-28% of drivers file glass claims every 3 years. Average replacement costs run $300-450 for standard vehicles and $600-900 for vehicles with ADAS systems. They calculate the expected annual cost per driver, add administrative expenses and profit margin, and arrive at the premium.

Sample Arizona calculation: 25% claim frequency multiplied by $400 average cost, divided by 3 years, equals $33.33 expected annual cost per driver. Add $20-40 for administration and profit. Total embedded premium: $53-73 annually.

Why Pre-Paying Through Premiums Creates Value

There are four concrete reasons this model works in your favor.

Cost predictability. You’re paying a known $40-80 per year instead of absorbing a surprise $500 deductible when a rock kicks up on I-10.

Risk transfer. The insurer absorbs the volatility. You could need zero replacements or three in five years — your cost stays the same.

Prompt repair incentive. When there’s no financial barrier, drivers get chips fixed immediately instead of waiting until they spread into cracks that require full replacement.

Negotiated rates. Insurers negotiate shop rates lower than retail cash prices. You benefit from that collective bargaining power even though you never see the invoice.

What Does Zero-Deductible Coverage Actually Include?

When you file a zero-deductible glass claim, here’s what’s covered at $0 out-of-pocket:

Full Windshield Replacement

- Glass: OEM-equivalent meeting FMVSS 212 safety standards

- Labor: Removal, surface preparation, and installation

- Materials: Urethane adhesive and mounting components

- Mobile service: In most markets, the technician comes to you

- Moldings and trim: Replaced if damaged during service

Windshield Repair

- Chip repairs ($75-150 value per repair)

- Minor crack repairs where technically feasible

- Multiple repairs per policy period — no typical per-period limits

ADAS Recalibration (Increasingly Standard)

If your vehicle has Advanced Driver Assistance Systems — and roughly 68% of current vehicles do — ADAS recalibration is increasingly covered as a necessary component of windshield replacement. Forward camera calibration runs $150-250. Multi-sensor systems can reach $300-400. Without recalibration, your lane departure warnings, automatic emergency braking, and adaptive cruise control won’t function correctly.

Additional Glass Coverage (Policy-Dependent)

Many policies extend zero-deductible coverage to side windows, rear windows, quarter glass, and sunroof glass. Always verify your specific policy.

What’s Typically Excluded

Cosmetic damage not affecting safety (minor pitting, wiper-caused surface wear), pre-existing damage that existed before your policy started, aftermarket modifications beyond factory specs, and intentional damage by the policyholder or household members.

What Does “Free” Glass Really Cost in Arizona?

Arizona’s zero-deductible glass situation is unique nationally. It’s not an optional endorsement — it’s market standard. About 85% of comprehensive policies include it automatically. You don’t check a box or pay extra. It’s embedded in your base comprehensive premium.

Why Arizona Developed This Standard

Desert conditions drive it. Extreme temperatures cause rapid crack propagation — a small chip in Phoenix can become a full replacement within days. Highway truck traffic on I-10 and I-17 generates constant debris exposure. Glass claims represent 22-28% of all Arizona comprehensive claims, compared to 12-15% nationally. Insurers compete by offering generous glass coverage rather than fighting inevitable claims.

True Cost Analysis for Arizona Drivers

Let’s run the numbers on a hypothetical $400/year comprehensive policy.

With zero-deductible glass (standard): Base comprehensive premium: $400/year. Embedded glass coverage cost: approximately $50/year. Explicit additional cost: $0. Total: $400/year including glass.

Without glass coverage (hypothetical): Base comprehensive: $350/year. Out-of-pocket windshield replacement every 2-3 years: $400 average. Annualized replacement cost: $133-200/year. Total: $483-550/year.

Arizona’s zero-deductible glass provides $83-150 in annual value even after accounting for the embedded premium cost. And that’s before considering cashback.

Arizona Cashback Makes It Even Better

Arizona permits glass shops to offer cashback incentives — currently up to $375 with NuVision Auto Glass. These come from shop marketing budgets, not from your insurer. So your total service cost is $0 out-of-pocket, you receive up to $375 in cashback, and the net result is a positive cash flow event. Your windshield replacement actually generates income. That’s as close to genuinely “free” as insurance gets.

How Does Florida’s Zero-Deductible Glass Work After SB 1002?

Florida’s 2023 insurance reforms (SB 1002) changed the landscape. Before 2023, many Floridians had zero-deductible glass included in base coverage. Widespread fraud drove premium increases, and the law was reformed.

Current Florida Glass Coverage Structure

Repairs: Genuinely free. All Florida insurers must waive deductibles for windshield repairs (not replacements). This is state-mandated consumer protection. Your out-of-pocket cost for a chip repair: $0. No endorsement needed. No premium increase. This alone saves $75-150 per repair.

Replacements: Endorsement required for $0. Zero-deductible replacement coverage is available as an explicit endorsement costing $60-85/year. Without it, your standard $250-500 comprehensive deductible applies to every windshield replacement.

Value Analysis for Florida Drivers

High-exposure drivers (I-4, I-95, Turnpike commuters): Endorsement cost: $75/year. Typical replacement frequency: every 4-5 years. Deductible avoided: $500. Annualized savings: about $111-125/year. The endorsement pays for itself if you need replacement more often than every 6-7 years. For highway commuters in Tampa, Orlando, or Jacksonville, that’s a strong bet.

Low-exposure drivers (urban, limited highway miles): Endorsement cost: $75/year. Replacement frequency: every 8-10 years. Deductible avoided: $500. Annualized savings: about $55/year. Borderline value — it depends on whether you prioritize cost predictability over raw savings.

Is Zero-Deductible Glass Coverage Worth It in South Carolina?

South Carolina follows traditional insurance market patterns. Your standard $500 comprehensive deductible applies to glass unless you purchase a separate glass endorsement.

Regional Pricing Differences

Coastal (Charleston, Hilton Head, Myrtle Beach): $80-120/year endorsement. Hurricane debris risk, salt air degradation, and US-17 exposure make replacement within 5 years likely. Strong endorsement value.

Midlands (Columbia): $60-90/year endorsement. Mixed driving patterns create moderate exposure.

Upstate (Greenville, Spartanburg): $40-70/year endorsement. Lower debris exposure, but I-85 commuters still face significant risk.

Break-Even Formula

Divide your annual endorsement cost by the deductible you’d otherwise pay. That gives you the number of years to break even.

Upstate driver: $50/year endorsement, $500 deductible avoided. Break-even: 10 years. If you expect replacement within 10 years, the endorsement is worthwhile.

Coastal driver: $100/year endorsement, $500 deductible avoided. Break-even: 5 years. Given coastal conditions, most drivers recoup this easily.

Beyond Simple Break-Even Math

The break-even calculation doesn’t capture everything. Financial predictability matters — $60/year is plannable; $500 isn’t. ADAS-equipped vehicles face replacement costs of $600-1,200, which dramatically improves the endorsement value proposition. And if you’re already filing other comprehensive claims, glass endorsement prevents stacking high deductibles on top of each other.

What Are the Hidden Costs of Zero-Deductible Coverage?

While your out-of-pocket cost at service time is $0, some indirect costs deserve honest discussion.

Premium Increases Over Time

Zero-deductible glass premiums rise annually with inflation and claim trends. Florida and South Carolina glass endorsements increased 15-25% between 2020 and 2024. Arizona’s embedded costs increased proportionally. This is real — but it’s also true that cash replacement costs increased at similar or higher rates.

Opportunity Cost

If you never file a claim, those premiums represent money spent on coverage you didn’t use. You could theoretically choose a higher deductible, keep the premium savings, and invest the difference. However, the unpredictable nature of glass damage makes this comparison academic for most drivers.

Claim Pattern Risks

While 87% of single glass claims don’t affect insurance rates, excessive claims — four or more comprehensive claims within three years — may trigger rate reviews or non-renewal considerations. This is rare for glass-only claims but worth knowing. For more on how claims affect premiums, see our guide on whether auto insurance covers windshield replacement.

Quality Variations Between Shops

“Free” replacement through insurance doesn’t guarantee quality. Some insurers authorize the lowest-bid shop, which may use economy-grade glass or skip proper procedures. Verifying shop quality — certifications, reviews, warranty terms — remains your responsibility regardless of who’s paying.

When Does Zero-Deductible Coverage Fail to Deliver Value?

There are specific scenarios where the math doesn’t work in your favor.

Short vehicle ownership. If you buy a vehicle planning to sell within 1-2 years, paying $75-150 in glass endorsement premiums for coverage you’ll likely never use doesn’t make financial sense.

Older vehicles approaching end-of-life. A 15-year-old vehicle worth $3,000 may not justify ongoing endorsement costs if major mechanical failure is more likely than glass damage.

Garage-parked, ultra-low-mileage vehicles. If you drive 3,000 miles per year, park in a garage, and rarely take highways, your debris exposure is minimal. Over a decade, you could pay $800 in premiums for one replacement that saved you $500 — a net loss of $300.

Recently purchased coverage with immediate vehicle changes. If you add glass endorsement in Year 1, file a claim, then total the vehicle in Year 2, you still came out ahead on that specific sequence. But the second year’s premium was wasted.

When Does Zero-Deductible Coverage Clearly Pay for Itself?

The value proposition is strong for several driver profiles.

High-mileage highway drivers. Anyone putting 15,000+ annual miles on debris-heavy interstates — I-10, I-4, I-95, I-26, I-85 — faces frequent glass exposure.

ADAS-equipped vehicles. When your vehicle’s windshield replacement costs $600-1,200 including recalibration instead of $300-450, the deductible savings are significantly larger. Whether you drive a Toyota, Honda, Ford, Tesla, or Chevrolet, ADAS makes the endorsement more valuable.

Long-term vehicle ownership. Planning to keep your vehicle 5+ years maximizes the probability that you’ll file at least one claim.

Outdoor parking. Vehicles parked outside face higher exposure to hail, vandalism, falling branches, and temperature-related stress cracks.

Arizona residents. Near-certain value given extreme conditions and embedded coverage. You’re already paying for it — use it.

Benefits Beyond Dollar Savings That Most Drivers Overlook

The financial analysis only tells half the story. Several non-dollar benefits matter for real-world driving.

No decision paralysis. When a rock chips your windshield, you don’t have to weigh whether it’s “worth” fixing. The cost is already covered through your premium. You just schedule mobile service and move on.

Better safety outcomes. Zero-deductible encourages prompt chip repair, which prevents crack propagation. Chips addressed immediately don’t grow into sight-line obstructions. ADAS warnings get resolved quickly instead of being delayed over cost concerns. Your windshield is a structural safety component — keeping it intact matters more than most drivers realize.

Vehicle value preservation. Maintaining your windshield protects resale value. Documented insurance claim records demonstrate proper maintenance history. Visible cracks reduce trade-in offers.

Time savings. No shopping for cash quotes. No price negotiation. No spending an afternoon comparing shops. You file a claim, pick your shop, and the work gets done.

How to Maximize Your Zero-Deductible Glass Coverage

If you’re paying for it — and you are, through premiums — use it strategically.

Address chips immediately. Don’t wait for a small chip to become a long crack. File a repair claim the day you notice damage. Repair is faster, cheaper for the insurer, and keeps your windshield structurally sound.

Choose your shop carefully. Zero-deductible doesn’t mean accepting the lowest-quality service. Verify that your shop uses OEM-equivalent glass (not economy grade), includes ADAS recalibration when required, provides a lifetime workmanship warranty, and follows proper adhesive cure times.

Understand your full coverage. Know whether your policy covers side windows, rear glass, and sunroof glass. Verify that ADAS recalibration is included. Confirm whether mobile service carries any additional charge.

Monitor premium changes. Review your annual renewal for glass endorsement cost increases. If your endorsement jumps 30% in a year, shop competitor quotes that include glass coverage comparisons.

Arizona drivers: Use cashback offers. Take advantage of legal cashback incentives (up to $375 with NuVision) to turn a covered replacement into a net-positive financial event.

Florida drivers: Prioritize repairs. The mandatory repair deductible waiver is genuinely free — no endorsement required. Prompt chip repair prevents the need for costlier replacement.

Conclusion: “Free” Is Relative, But the Value Is Real

Zero-deductible windshield replacement isn’t truly free. It’s funded through insurance premiums that all policyholders pay collectively. Arizona drivers pay $40-80 annually embedded in comprehensive premiums. Florida and South Carolina drivers pay explicit $40-150 for optional glass endorsements.

But here’s what matters: this premium-funded model converts unpredictable $300-1,200 replacement costs into manageable, predictable annual expenses. For Arizona drivers, it’s essentially standard — you’re already paying for it, so use it. For Florida and South Carolina drivers, the endorsement breaks even with one replacement every 6-10 years, and most highway commuters beat that timeline easily.

The real value isn’t eliminating all costs. It’s risk transfer, financial predictability, and removing the barrier that causes drivers to delay addressing safety-critical windshield damage.

NuVision Auto Glass works with zero-deductible coverage daily throughout Arizona, Florida, and South Carolina. We verify your coverage, handle all insurer communication, and ensure you get maximum benefit from your policy — all while maintaining quality installation standards with OEM-equivalent glass, certified technicians, and proper cure times.

If you have zero-deductible coverage and windshield damage, use it. You’ve already paid for this benefit through your premiums.

Get a Free Quote From NuVision Auto Glass →

Frequently Asked Questions

If I have zero-deductible glass and never file a claim, did I waste money?

From a pure dollar perspective, yes — you paid premiums without receiving a direct payout. But insurance isn’t wasted just because you don’t file claims. You received risk transfer and peace of mind for the entire coverage period. Think of it like homeowners insurance in years without storms.

Can I drop zero-deductible glass coverage mid-policy to save money?

Usually yes, with a pro-rated premium refund. But if you drop coverage and then experience glass damage, you’ll pay the full deductible. Only drop if you’re confident in near-term vehicle disposition or have drastically reduced your driving.

Does zero-deductible glass cover damage I cause intentionally?

No. Insurance covers accidental damage only. Intentional damage by the policyholder or household members voids coverage and may result in policy cancellation and fraud charges.

Can I file unlimited glass claims with zero-deductible coverage?

There are typically no per-policy-period limits. However, four or more comprehensive claims (including glass) within three years may trigger rate reviews or non-renewal considerations with some insurers.

Does “free” glass mean I can upgrade to luxury windshield features?

No. Coverage includes OEM-equivalent replacement matching your vehicle’s original specifications. Upgrades like enhanced tinting, acoustic glass, or hydrophobic coatings beyond factory specs require out-of-pocket payment for the upgrade portion.

If my windshield was damaged before I added zero-deductible coverage, is it covered?

No. Pre-existing damage isn’t covered. Insurers may request photos when you add coverage or file claims shortly after adding a glass endorsement to verify there’s no pre-existing damage.